Starting a business is a risky endeavour.

You can put in long hours, invest your hard-earned money, and pour your heart and soul into it – only to watch it fail.

Unfortunately, this is the reality for many entrepreneurs.

In fact, according to research, 20% of all new businesses are unsuccessful in the first two years.

That’s one out of every five businesses that don’t make it past their second year!

But that doesn’t have to be your reality, so don’t give up hope.

Some factors will always be beyond your control, such as economic downturns.

But there are several strategies you can use to make sure your small business not only survives but thrives!

In this article, I’m going to delve into the 10 biggest reasons small businesses fail and how you can prevent that from happening to you.

#1. Poor Financial Management

Poor financial management can kill your cash flow and make it challenging to pay bills when they are due.

Late payments can then result in late fees, penalties, and damaged relationships with suppliers and vendors.

If you have trouble keeping a close eye on your business finances, you can end up paying too much on rent, utilities, and office supplies.

Without a proper budget, you may even spend more than you can afford, which can lead to financial difficulties down the line.

Solution: Start by creating a budget for your business and sticking to it. Keep accurate financial records to track income, expenses, and profits. This will help you make informed financial decisions and identify areas for improvement.

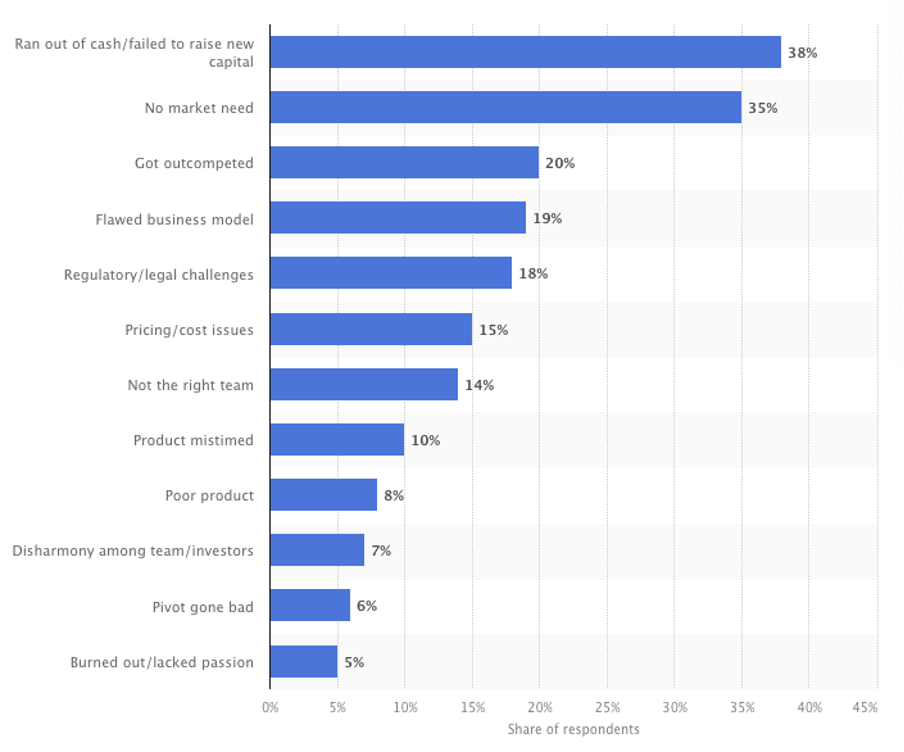

#2. Running Out of Money

Running out of money is the top reason why most small businesses have to shut down.

77% of small businesses worldwide rely on the owner’s personal savings to fund their business in the early days.

But when you need a cash infusion to test the market, there’s only so much your savings can supply.

Small business owners often face cash flow issues after exhausting their savings.

It becomes such a massive problem they have to close their doors or go bankrupt.

Solution: Develop a cash flow forecast that predicts the business’ inflows and outflows for the coming months. Keep an eye on account receivables to ensure your customers pay on time. If you sell physical products, maintain optimal inventory levels.

#3. Failing to Pivot

To be successful, all businesses need to be able to adapt to market conditions.

If you cling on to your original business idea, even when it fails to find a market, can make your business a loss-making enterprise

Staying flexible and adjusting course when necessary is the secret to success.

Many of today’s successful businesses are very different from how they started.

For example, Starbucks originally sold coffee makers.

Instagram started as Burbn (a check-in app).

Netflix launched sending DVDs by mail, then pivoted when streaming made DVDs almost obsolete.

Eventually, every brand will pivot to adapt and survive in changing market conditions.

Solution: Be prepared to let go of your original business idea if your business is struggling or the market is changing.

Don’t be afraid to pivot to a new product or service your customers want.

You may even have to adopt a new business model.

Like changing from single sale transactions to recurring subscriptions.

Remember what happened to many offline businesses during the Covid-19 pandemic?

Many had to move online or add take-out and delivery options.

You need to be agile and ready to do something like that.

#4. Ineffective Business Planning

If you overlook the importance of business planning, it’s tough to achieve your goals.

Without a clear understanding of your business goals and objectives, it’s hard to make informed decisions.

Planning is also needed to develop effective strategies for growth.

Solution: Build a realistic plan based on present and future sales projections.

You don’t need to have a complicated plan, but make sure it includes the following:

- Business vision, mission, and goals

- Market research and competitive analysis

- Employment needs

- Potential problems and solutions

- Capital needs for all business operations

#5. Inventory Mismanagement

Inventory mismanagement is a novice error that any small company can make.

It is critical to forecast so your product supply can meet demand.

Inefficient inventory management often leads to a significant shortfall in cash flow.

You will either end up with too many products or not enough, leaving you unable to meet customer orders.

Holding excess inventory can also result in increased storage costs.

If your stock has a finite shelf-life, excess inventory can also result in waste.

Solution: Conduct monthly audits and find the balance between supply and demand. Do this to avoid excess inventory, obsolete products, or early sellouts.

An inventory management software like Netstock, Sortly or Extensiv can help you automate and optimize the whole process.

Pro tip: Put in place a Just-in-time (JIT) inventory system to order products as needed rather than keeping large quantities on hand.

#6. No Online Presence

About 2.56 billion people worldwide shop online, and the number keeps increasing.

The digital age has forced many businesses to switch from an offline to an online business model.

Online marketing is more cost-effective than traditional methods.

You can use social media, email marketing, and online advertising to reach your target audience within a small budget.

Solution: Create a simple website that educates your target audience about your product and creates an online ordering funnel. If you don’t have the time and resources to create a website, simply sign up for a marketplace like Amazon or Etsy and start selling.

#7. Trying to Do It All

When you start, you might find it hard to hire people and trust them with your day-to-day business operations.

But to grow, you must learn to delegate.

Don’t try to be a jack of all trades.

You can’t be an expert at everything, and you have a finite number of hours each day.

Solution: Delegation is the best technique to expand and protect your business from failure. But remember, hiring isn’t the only solution. You can even invest in software that helps automate processes and save time.

#8. Unable to Cope with Customer Expectations

If your business cannot meet customer expectations, it can cause them to lose their trust in you.

People will switch to a competitor if they think you can’t meet their needs.

Dissatisfied customers might also leave a negative review or worse.

They may share their negative experience with their friends and family.

Poor word-of-mouth marketing will put a stain on your reputation.

Solution: Understand customers’ needs by talking to them and make your business model fit.

Providing excellent customer service is vital to meeting customer expectations.

Ways to improve customer service include;

- prompt responses to enquiries,

- addressing complaints in a timely and professional manner

- going above and beyond to exceed expectations.

#9. Not Hiring the Right People

Most small businesses fail to hire the right talent due to limited resources, a small network, or a lack of hiring skills.

Hiring mistakes can lead to:

- Decreased work productivity

- Low employee morale

- Lower employee retention

Solution: If you’re not a hiring expert, bring an HR manager on board. Focus on finding candidates who are eager to learn and are a right fit for the job and company culture.

Pro tip: Ensure that you focus on employee retention after hiring.

#10. Fear of Business Failure

Are you afraid to try new tactics or jump on promising opportunities?

If you’re worried you will fail, you will become overly cautious and avoid taking risks that might help your business grow.

Fear of risk leads to a lack of innovation and creativity.

Don’t be afraid to try non-traditional strategies and explore new markets.

Solution: Learn how to embrace failure as a learning opportunity. Look back at your mistakes and identify ways to improve. Maintain a positive mindset and focus on your strengths and accomplishments.

Set for Success

There’s no reason you can’t grow a successful business and avoid the hurdles that have knocked down others.

Sure, success isn’t guaranteed.

But when you persevere and follow the solutions and tips in this article, you’ll be able to tackle any challenge that comes your way.

The result?

A sustainable business that you can build and scale for years to come.